![]() Purchasing a home will always be a stressful process, but there are steps you can take to make it a little less painful. When I purchased my first home at age 21, I wasn’t nearly as informed as I am now, which resulted in a few costly mistakes. With the first-time homebuyer’s experience behind me I am in the process of purchasing another home. The accounting and finance background I now have, have been tremendous tools in helping me to purchase a home in the most cost-effective method for my financial circumstances. Here are the six strategies I learned that make purchasing a home a little easier.

Purchasing a home will always be a stressful process, but there are steps you can take to make it a little less painful. When I purchased my first home at age 21, I wasn’t nearly as informed as I am now, which resulted in a few costly mistakes. With the first-time homebuyer’s experience behind me I am in the process of purchasing another home. The accounting and finance background I now have, have been tremendous tools in helping me to purchase a home in the most cost-effective method for my financial circumstances. Here are the six strategies I learned that make purchasing a home a little easier.

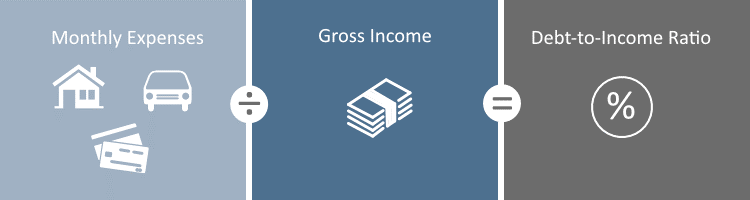

1. Know what you’re getting into

Create a spreadsheet that lists your balances and monthly payments, then calculate your DTI (debt-to-income) ratio. Knowing your current DTI will help give you an estimate on how much you will be pre-approved for and provide a rough estimate on the monthly cost of your mortgage. Most programs require your DTI to be under 40%, including your mortgage balance.

Source: https://www.rubyhome.com/home-loans/debt-to-income-ratio-dti/

2. Do your research

There are different loan programs available in Alaska depending on where you purchase a home, your income level, military service, the type of home you are purchasing (single vs. multi-family), and your ethnicity. Comparing all the programs you are eligible for will help you find the most cost-effective option. In some cases, just because the interest rate is lower with one program there may be additional costs making that program more expensive in the long-run. Choosing a program with a higher interest rate but lower backend costs may be a more cost-effective choice than the low interest rate program with more costs. So, pay attention to the APR and terms of each program!

3. Check your credit score

3. Check your credit score

Checking and staying on top of your credit score is easier than ever because “There’s an App for that!” I personally use Credit Karma, however there are multiple companies such as Mint and even banks such as Bank of America giving people the option to check their credit score for free. Credit Karma provides me with my TransUnion and Equifax scores and shows all the accounts I have ever had opened. It also notifies me when new accounts are opened or closed, which is a convenient way for me to monitor fraudulent activity and possible identity theft.

4. Know the market

Start looking at the market and housing prices a few months in advance before you even start the pre-approval process. This will help you to stay informed on which areas may be priced more competitively, the houses in your price range, and which houses are reasonably priced and sell quickly versus those that stay on the market for longer. Another trick I learned is that a house that was pending but has come back up on the market for sale, most likely has an inspection report already done. Sellers are motivated and don’t want to go into contract with you if you are going to back out after you find something on the inspection report you don’t like. As a result, they are normally willing to give you the inspection report to view before putting an offer in. Viewing the inspection report will give you an idea on the overall condition of the home and will better inform you in selecting an offer price.

5. Pay attention to interest rate trends

Watching interest rate trends will help you decide if you should lock your rate in as soon as you find a home, or if you should wait for the possibility of interest rates to dip. Knowing when to lock in is a tricky game, but if you have a knowledgeable lender they should be able to provide you with advice. Also keep in mind that depending on the program you use, the time you can lock into your rate will vary. This could be another factor when choosing a loan program. I compared two programs and chose the one that gave me a 60-day lock period versus a 45-day lock period because I believed interest rates were on the rise and that the sellers were going to take over 45 days to close. Each person’s scenario is different, and you should always weigh all the factors.

6. Watch your spending!

Once you are pre-approved, do not increase your spending habits or take out new credit. Your pre-approval rate is based on your current DTI. If your DTI increases, that may decrease your approval amount. Keep your credit card debt the same or minimize it, do not take out any new loans, and maintain or increase your cash cushion. Once you find a home and the underwriting process begins, they will check all the information you gave them to make sure nothing has significantly changed. I have heard numerous stories of people purchasing new furniture or appliances on credit before they have closed on their home, then running into issues with underwriting. In the worst-case scenario, the new appliances or furniture they bought on credit for their new home prevented them from closing and purchasing the home. The irony of having brand new furniture and no home to put it in!

Remember each person’s scenario is different and there are many factors involved with purchasing a home. These are the tricks that have helped me smoothly purchase a home and can hopefully help you next time you are in the market for a new house. Happy Home Shopping!

Jasmine Gilpin

Associate Financial Advisor

10/10/18