As everyone is talking about ROTH conversions opportunities in 2020, in the midst of a pandemic, it is time to revisit this strategy and answer the “why now” question. While ROTH IRA contributions still have contribution and income limits, ROTH conversions have neither an income limit on being eligible to convert, nor a limit on how much you are allowed to convert.

The advantage of ROTH over traditional can be summed up pretty quickly:

| Attributes: | Traditional IRA | ROTH IRA |

| Taxation on Growth | Tax-deferred | Tax-deferred |

| Required Minimum Distrubtions (RMDs) | Yes | No |

| Taxation on Withdrawals | Ordinary Income | Tax-free (potentially) |

As we have stated in prior articles on ROTH conversions, particularly this blog shortly following the passage of the Tax Cuts and Jobs Act, https://www.akwealthadvisors.com/blog/financial-planning/time-now-roth-conversions/, there are many advantages to including ROTH IRAs in your retirement strategy. Not only did TCJA make the strategy more appealing from a tax standpoint, but the pandemic of 2020 has added to the appeal as a result of the following:

- Taxable income might be lower in 2020. For example, RMDs have been completely waived. Sources of ordinary income might be down such as employment or rental income.

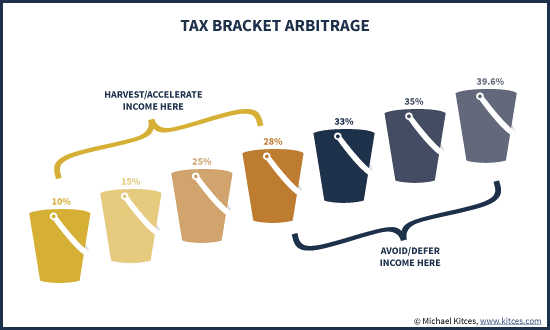

- Thanks to TCJA, tax rates are lower than in 2017, but due to sunset in 2025 (or sooner?). Convert now to avoid worrying about future tax rates possibly being higher. Check out this chart from kitces.com about filling up these lower tax brackets:

- Most importantly, IRA account values are probably lower as a result of market impact. Converting while the values are down is a bargain, as the taxable amount is lower and the rebound is experienced tax-free in the ROTH.

Keep in mind that whatever you convert is included in ordinary income and taxed in the year of the conversion. ROTH conversions are excluded in some tax calculations, such as whether you are still eligible to contribute to an IRA. For the most part though, you have to be able to estimate your tax bracket for 2020 to determine which brackets you are filling up and the impact on your other tax calculations, such as social security taxation, Medicare IRMAA charges, net investment income tax (NIIT), and all sorts of other caveats that your tax advisor knows best. Work with your tax advisor and your financial advisor (that should be us) to determine the optimal amount, taking into account your entire tax picture and investment accounts.

Remember, these are long -term funds. Do not convert money you need to use in the near future. The ROTH IRA has a 5-year clock and other rules to be aware of for full tax benefits, but these are pretty easy to meet for long-term investors. The good news is that conversions are not an all or nothing proposition, you can do partial amounts – whatever amount is appropriate for your tax situation. Or perhaps not appropriate at all. The important thing to remember is that you can convert, but you cannot undo, so this is an irrevocable decision.

To make the conversion most effective, the taxes due for the conversion should be funded out of other money in your after-tax accounts/savings. Otherwise, the circular equation for paying the taxes on the conversion from the IRA might negate the benefits.

In summary, lower market values now and potential higher tax brackets in the future bode well for ROTH conversions in 2020.

Cathie Straub, CPA, CFP®

Director, APCM Wealth Management for Individuals

5/1/2020