I’m sure many of you have read news headlines stating that companies are having a hard time finding workers to not only fill job roles, they are now having to compensate them more to retain or hire. U.S. Job Openings represented by JOLTS attempts to measure how many unfilled jobs there are currently in the U.S. August was at 10.9 million, which is currently an all-time high. This ironically happened when the U.S. has roughly 5.33 million less people employed compared to pre-Covid levels. As a result, household names such as Walmart and Amazon have both increased wages as the bidding war for workers has heated up. They are not by any means the only companies that have had to increase compensation expenses. The rest of this writing will focus on wage growth in hopes to explain what is driving this increase, what other factors should be considered, and what impacts this could have for markets and corporations.

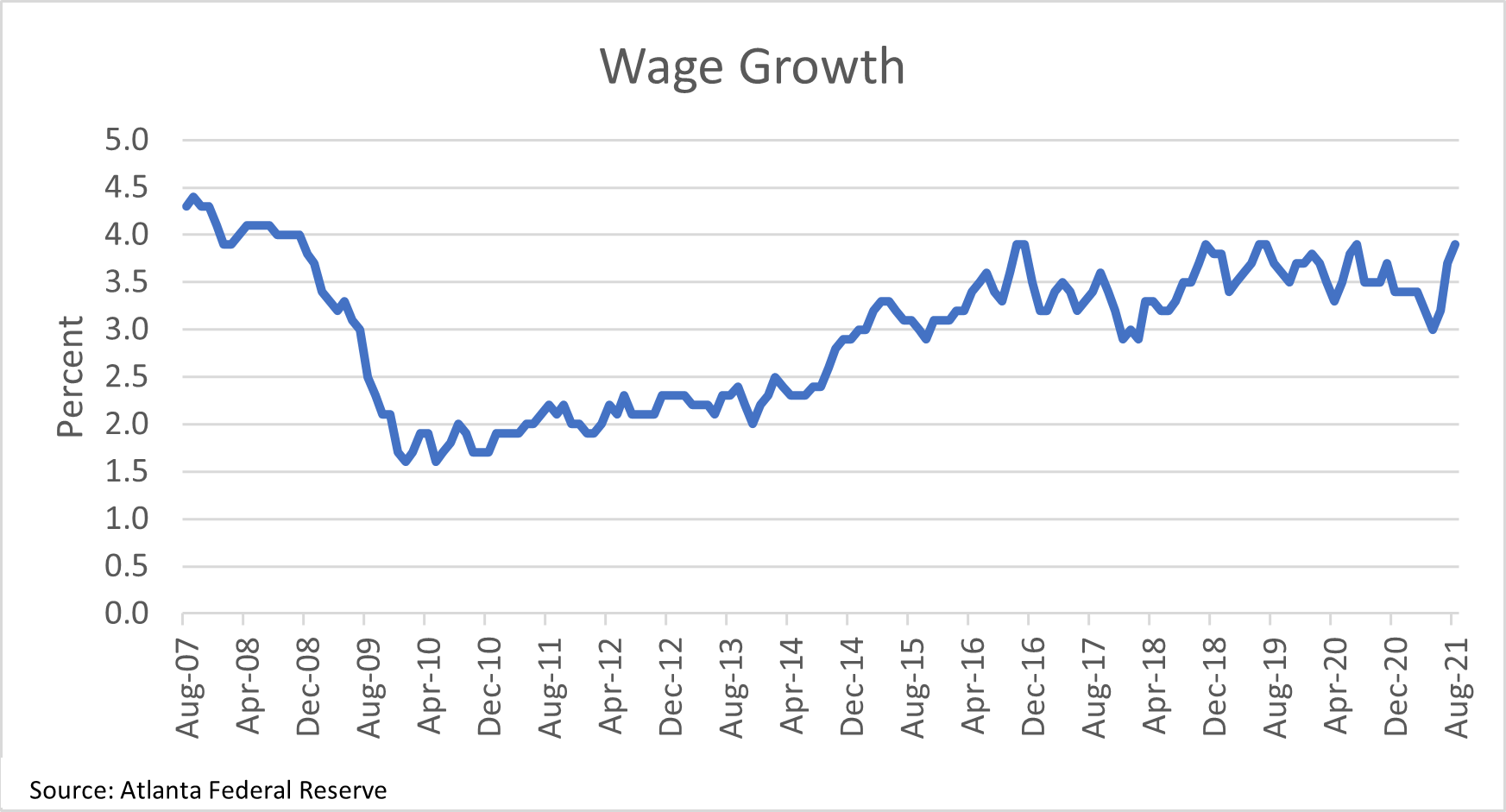

There are multiple ways to measure wage growth, however shown below is data compiled from the Atlanta Federal Reserve (AFR). The AFR measures wage growth using a median 3 month moving average based on the nominal wage growth of individuals based on microdata and Current Population Surveys (CPS). The most recent growth number was 3.9% for August which has been tied for highs dating back to 2008. I believe the increase in wages also referred to as “Wage Inflation” cannot be isolated to one policy decision or one structural change, but more likely the combination of multiple factors driving this increase. The increased unemployment insurance (UI) has certainly helped discourage some workers from reentering the labor market. The extra UI supplement ended in the beginning of September for states who hadn’t already cut the program which makes it too early to have enough data supporting the fact that once that has completely ended more workers will reenter the labor market. Hopefully this will begin to fill the gap in the labor shortages which are in part driving the growth in wages. The structural change and potentially the most important factor has the been the acceleration of adopting new technological progress. Mainly allowing the ability to work from home or anywhere for that matter. This has resulted in workers being more productive shown by the increase in nonfarm business productivity which increased by 2.1% in the 2nd quarter of 2021 according to the U.S. Bureau of Labor Statistics (BLS).

Other factors to consider such as the Unit Labor Cost (ULC). This measures the average cost of labor per unit of output produced, has also increased. BLS reported an annual increase of 1.3% in ULC of which was made up by a 3.4% increase in hourly compensation and a 2.1% increase in productivity. Typically, as workers become more productive, they demand more compensation usually in the form of wage increases. Wage increases tend to fall into the bucket of inflation called “sticky inflation”. This type of inflation is significantly more difficult to reverse once it occurs, whereas “transitory inflation” tends to subdue mainly when supply and demand problems are resolved. However, if hourly compensation increases with labor productivity the impacts can be less harmful for corporations and economic growth. It will be important to monitor this data going forward for the potential impacts this could have on the economy. BLS is scheduled to release the 3rd quarter data on November 4th, 2021.

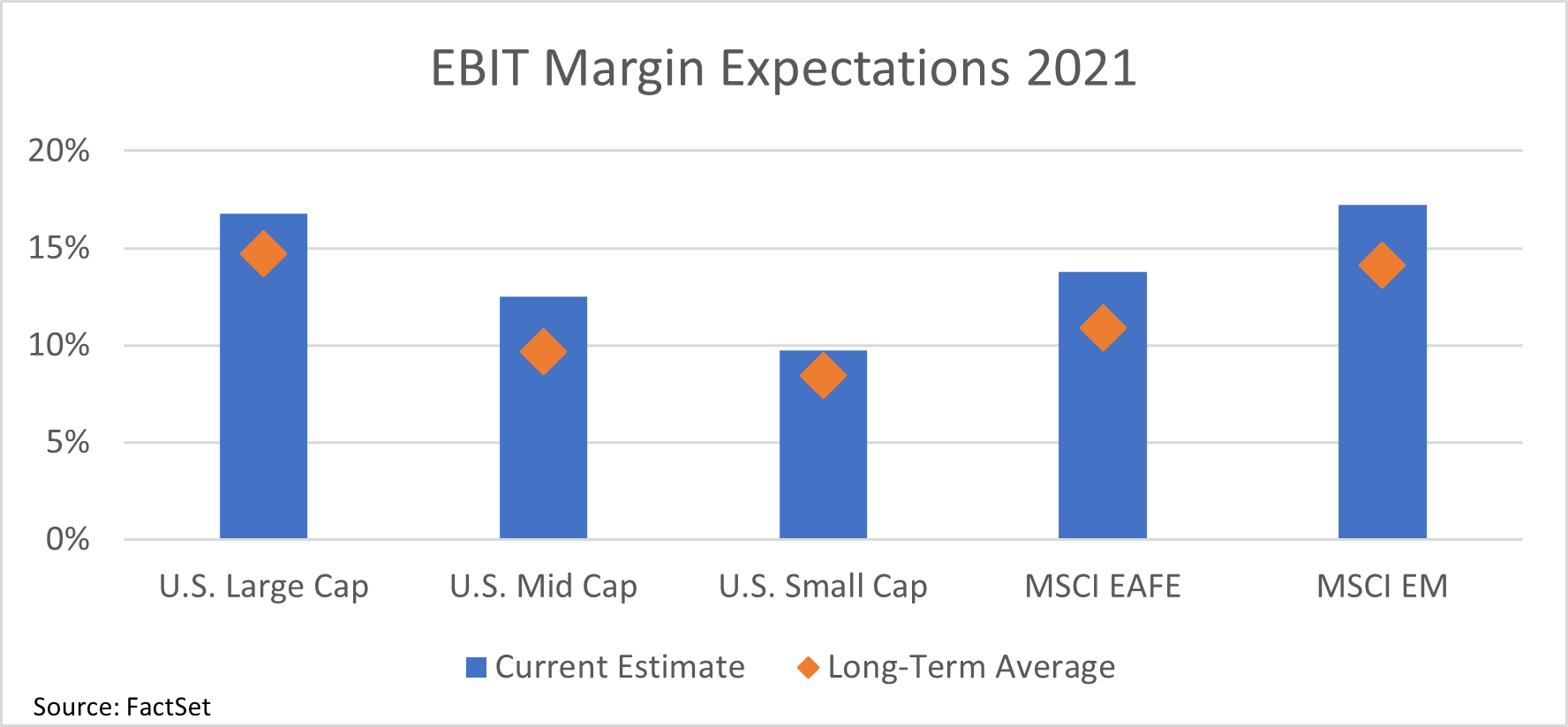

Does wage inflation matter for corporations and markets? Initially many would think “yes,” clearly this will hurt corporations’ margins, in particular the operating margins, however generally it has not. Corporations have continuously passed these costs along to the consumers in the form of higher prices to avoid eroding margins and there is no reason to suspect this won’t happen again. EBIT margins are forecasted to remain above long-term averages through 2021 across the globe as shown below.

Conclusion

Wage inflation is sticky (not likely to reverse) and isn’t necessarily a harmful type of inflation for the economy and corporations if productivity continues to increase which will be monitored in the future. Productivity slowing mixed with wage inflation increasing could squeeze margins and bottom lines. Corporations will attempt to pass on the extra expenses associated with compensation increases to consumers in the form of price increases to maintain these healthy margins. Monitoring this going forward will be two-fold. Will productivity continue to increase with wages in the third quarter and on? And will corporations be able to maintain margins by passing on costs going forward?

Jack Straub

Investment Analyst

10/4/2021