Pandemic

The path of the virus continues to be the key contributor to the near term economic and financial market outlook. Unfortunately, COVID case growth is accelerating again around the world, particularly in the U.S. and Europe.

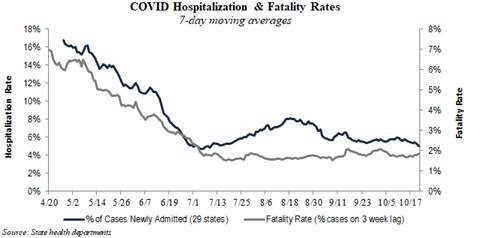

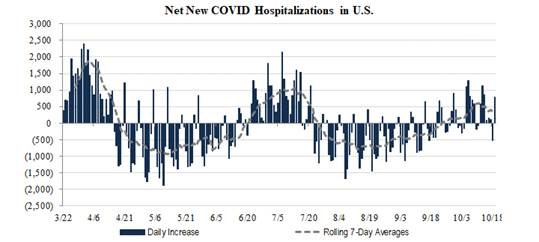

- A surge in case growth is tolerable and should not significantly derail the economic recovery as long as deaths and hospitalizations remain low. This conclusion is predicated on the thought that individuals will adjust their mobility and economic participation based upon their perception of severity should they contract the virus. Importantly, hospitalization and death rates remain low relative to early spring (chart 1 and 2) which may be attributed to the identification of effective methods of treatment as medical professionals learn more about the virus and the efficacy of available medications (Remdesivir, Dexamethasone) . Additionally, case growth has been concentrated in the younger population. It is interesting to note, the second wave we experienced in the summer brought about lower hospitalization rates than the first wave in the spring. The hope is the current wave of increased hospitalizations will be a third lower high. Case growth is still accelerating though, so it’s early to call for a peak in hospitalizations.

- It is plausible that we could simultaneously experience higher case growth and higher economic growth if people are in fact learning to protect at-risk populations while the rest of society is going about its business. If that is true, it implies stronger economic growth and higher case growth. As long as hospitalization and death rates remain low the economic impacts of this third wave could be minimal.

- We are cautiously optimistic that the re-acceleration in case growth will have a minor impact on the current economic expansion. Our friends at Evercore ISI have trimmed their US real GDP forecast for 4Q from +10% to +8%. The new economic and social restrictions taken in Europe and parts of North America will slow the pace of recovery but recession risks are much smaller than the economic plunge in the second quarter. Trends in near term hospitalization and death rates will impact this view.

Politics

Biden is still favored to win the election, but polling in some key battle ground states have narrowed. The U.S. election race, and its impact on much needed fiscal support, will dominate market action through at least early November.

- The makeup of Congress is very important as it impacts the President’s ability to push meaningful legislation. Democratic clean sweep odds– taking the White House and Senate while maintaining the House – are down to 56% as some battleground Senate races have tightened up. In a democratic sweep probabilities of a larger 4th fiscal package ($2.5-$3T) will increase providing momentum for the economic recovery which in turn could pull forward the Fed’s first rate hike. Under a blue sweep, the political outlook for domestic equities is neutral given the combined effects of higher corporate tax rates, more fiscal stimulus, and lower tariffs.

- Even though the polls show a steady advantage for Joe Biden in the Presidential election it doesn’t mean that Donald Trump can’t win. A divided government (D-R-D or R-R-D) is unlikely to deliver meaningful legislative change. Investors should expect a more reactive approach to fiscal stimulus if the economy requires further aide induced by a substantial downturn in economic activity or weaker markets. In the near term, equities may come under pressure to embed a risk premium associated with additional fiscal stimulus. But, already ample liquidity and expectations for an upturn in the business cycle will support corporate earnings and domestic equities.

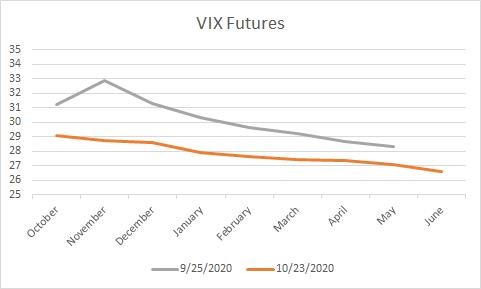

- A contested election result is still a distinct possibility given the tightness of the polls in key swing states. The uncertainty around the timing of the election result, and the outcome of the election itself is pushing VIX futures (market’s expectation of future volatility) higher. Although these levels are still elevated they are lower relative to the end of September suggesting some investor complacency (chart 3).

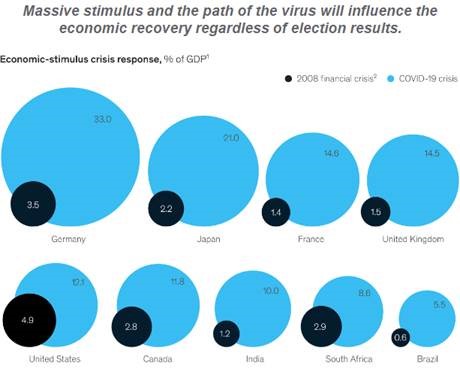

- The election will inevitably contribute to market volatility in an already complex and uncertain world, But, the overall economic trajectory will be impacted by the path of the virus and massive global policy support regardless of election results. The US policy response in this crisis is almost 2.5x larger (Chart 4 stimulus as a % of GDP) than what occurred during the Global Financial Crisis! This is a large tailwind for the continuation of economic healing into 2021.

Portfolio Positioning

- Last week, the Beige Book (Federal Reserve Bank information on current economic conditions) reported that economic activity grew in “all” Districts since September but some Districts modestly accelerated while others appeared to lose some momentum. Though hiring and wage growth were positive and inflation weak, some firms continued to lay off or furlough workers and some supply-constrained prices, like food, grew appreciably. The conclusions are consistent with a recovery that continues to advance in broad strokes but inconsistently and with less forward momentum than during the initial powerful rebound in May. The lull in fiscal stimulus and renewed broad-based surge in Covid-19 cases are undermining growth prospects but other economic releases suggest growth remains solid for 4Q.

- In China, third quarter GDP came in +4.9%, higher than the same quarter last year! China is the only economy of any significant size that will likely record positive growth for 2020 as a whole. It is difficult to exaggerate the impact of Chinese economic growth on the global economy. According to the IMF, China accounts for 18% of global GDP (in nominal U.S. dollar terms) and China’s economy will be 14% larger than its pre-pandemic levels by the end of next year. According to the WEO when 2020 and 2021 are taken together, global GDP will have expanded by some US$3.5 trillion on a net basis, and 60% will have been generated by China alone.

- When interest rates fall to zero, the ability for monetary policy to influence aggregate demand is weaker. This is because the connection between monetary policy and the economy is interest rates. When rates fall to zero, the link is severed. At this point, fiscal policy is a more effective way to revive aggregate demand, drive up economic growth and prevent price deflation. Fiscal package 4 negotiations continue, but political analysts suggest the discussions are a show meant to blame the other side for failure. After the election, the 4th fiscal package will likely pass lending the needed economic support until a vaccination propels a self-reinforcing expansion.

- Importantly, fiscal expansion tends to drive up economic growth and corporate profitability first, while the Fed continues to hold down interest rates. Inflation will be slow to come by until the economy begins operating at or near full potential. As a result, stock prices will be supported. Given this back drop we are choosing to look through near term election volatility and remain neutral on stocks vs. bonds but are underweight cash. We are holding modest tilts towards high quality large cap US stocks and industrial REITs.

Brandy Niclai, CFA®

CIO, Multi-Asset Strategies

10/26/20