One of the significant components of the $1.9 trillion American Rescue Plan (ARP) is the allocation of $350 billion to help states and municipalities cover the unexpected costs and offset the pandemic’s impact on their revenues. These funds will be paid directly to state and local governments. It comes in addition to $150 billion from the CARES Act, $500 billion provided by the Municipal Lending Facility and additional funds for schools, transit, housing, health care, stimulus checks, child tax credits and enhanced unemployment.

This financial support has been very important to the municipal bond sector. Without it, many governmental entities would have experienced significant financial challenges which would have meant increased risks to municipal bond holders. Since a year has elapsed from the start of the pandemic, most municipal issuers have closed one fiscal year and budgeted for the next. With direct stimulus from ARP, governments at all levels can use the funds to fill funding gaps created by the pandemic and adjust to the new normal as the economy opens further.

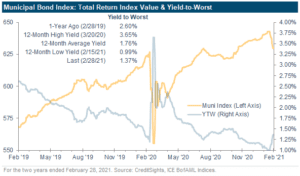

The effect of all this support is that in general, municipal budgets are unlikely to be significantly impaired by the pandemic. For holders of muni bonds, after experiencing pandemic induced volatility, the muni asset class has shown year-over-year profitability.

Looking forward, President Biden’s tax plan may provide pressure for muni yields to remain low. This is because it contains an increase in personal tax rates for high-income individuals. While it remains to be seen what changes to the tax code will actually pass Congress, a rise in personal tax rates should cause more money to be invested in tax-exempt municipal bonds as demand increases for tax-sheltered investments. As funds move into the space, yields would be pressured lower relative to other fixed income investments.

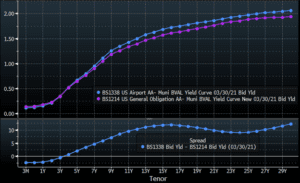

APCM continues to maintain its preference for muni bonds which are secured by the General Obligations of a governmental entity or by specific revenues such as water/sewer fees, school district tax receipts, or utility bills. While we have generally avoided bonds whose revenue streams have been impacted by the pandemic (e.g. sales taxes, toll roads, etc.), since the start of the year we have opportunistically initiated a few bonds secured by airport revenues. Not only have airports seen financial support from the U.S. government, but passenger count has been steadily rising and many airports have a significant amount of reserves that they can draw upon in the increasingly unlikely event that they experience a financial shortfall while waiting for the economy to return to normal.

Municipal Airport AA- rated bonds are currently yielding about 10 basis points more than General Obligation bonds for maturities over 10 years.

Source: Bloomberg

Paul Hanson, CFA®

Portfolio Manager

5/3/2021