![]() A couple of weeks ago I was thrilled to find out that I would be part of a small group of ten industry professionals from around the world that would participate in a 30-minute Q&A with Janet Yellen.

A couple of weeks ago I was thrilled to find out that I would be part of a small group of ten industry professionals from around the world that would participate in a 30-minute Q&A with Janet Yellen.

As I was preparing to leave Alaska to make the long trip to Toronto, I shared this exciting opportunity with my sister who promptly responded, “Who is Janet Yellen?”. Disappointed by her reaction I decided I must share my experience with readers who can truly appreciate an opportunity to meet the former Federal Reserve Chairwoman in person!

You can imagine that 30 minutes goes by quickly, so I was prepared to jump in as soon as an opportunity arose. Before I share my question let me provide some background.

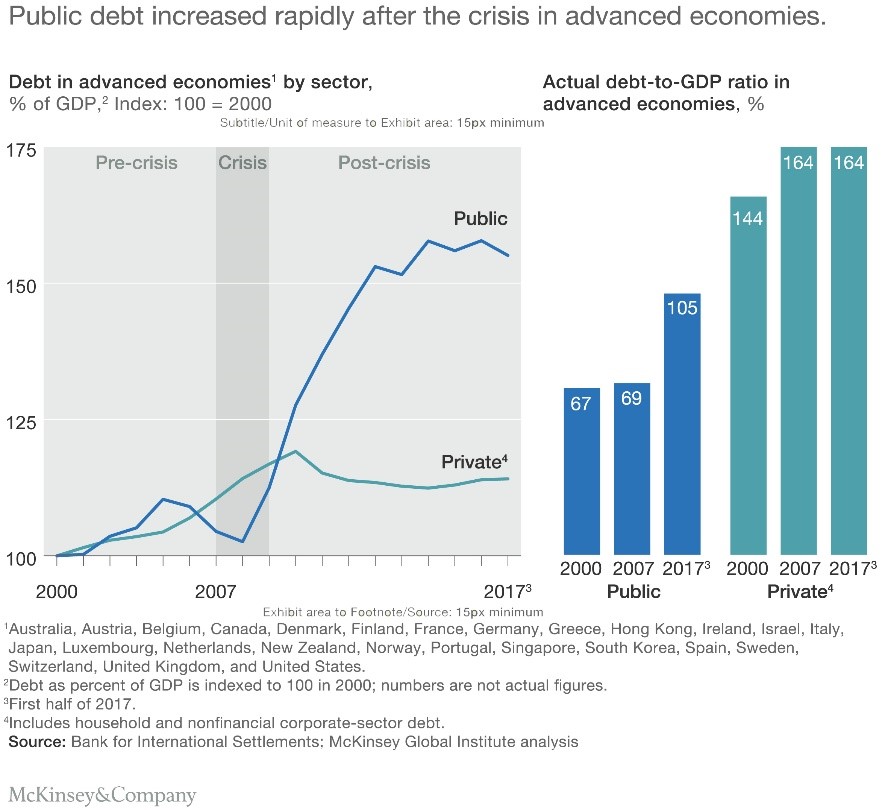

There has not been a movement towards deleveraging since the Global Financial Crisis. In fact, a recent report by McKinsey & Company noted that the combined global debt of governments, nonfinancial corporations, and households has grown by $72 trillion dollars since the end of 2007. China alone accounts for more than one-third of the debt growth and as illustrated in the chart below, debt has shifted to the public sector.

Current debt levels are of interest because debt is a headwind for growth, which we acknowledge in our secular (long-term) outlook expectations for modest economic growth. Some policy experts also believe the macroeconomic impact of tighter monetary policy could be larger than in the past, given the size of global debt.

So, I asked Janet if she concurred with this idea that the impact of tighter monetary policy could turn out to be larger than in the past. She does believe that the linkage between debt and monetary policy is greater today, which is one factor supporting the view that normalization in highly indebted countries should proceed very cautiously.

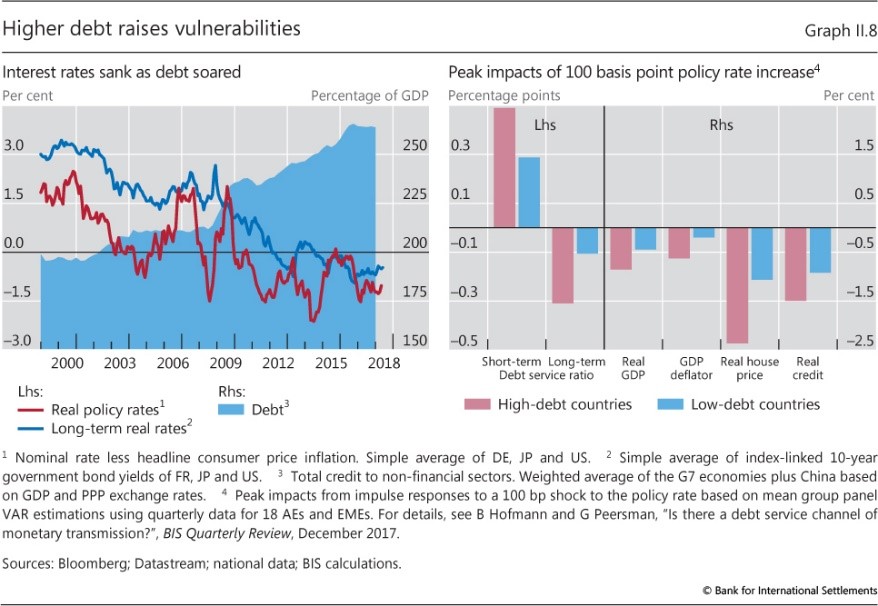

In fact, a recent report by the Bank for International Settlements draws the same conclusion.

Other participants theorized that countries with high debt levels should have lower neutral rates (the Federal Funds rate that neither stimulates nor restrains economic growth) relative to less indebted countries.

The challenge is that the downward trend in real rates and the upward trend in debt over the past two decades could be related and even mutually reinforcing. Low rates encourage debt accumulation and in turn, high debt makes it harder to raise interest rates. If the economy is more sensitive to the Fed changes in short term interest rates, then other tools will be needed to respond to the next economic downturn.

Janet did discuss the need for more tools in the Fed’s tool box. You can read about her support for pursuing a “lower-for-longer” strategy here.

This is just one of the challenges policy makers must face as they unwind the massive support provided after the crisis. These thoughts and challenges are debated amongst members of APCM’s investment committee during our strategy meetings. Our goal is to create thoughtful and realistic forward-looking assumptions to help our client’s build resilient portfolios.

If you made it all the way to the end of my comments I have three conclusions for you. First, you now understand why APCM believes we can live and work in the state we love and still connect to leading industry experts and policy makers. Second, we know the path to policy normalization will be challenging and the ride can get a bit bumpy, but we will factor this into our portfolio decisions. And third, unlike my sister you know who Janet Yellen is!!

Brandy Niclai, CFA®

CIO Multi-Asset Strategies

10/3/18