Bottom Line: Cash has historically had a bad rap in portfolio construction (i.e. cash drag and other negative terms) – but with interest rates set to rise and bond prices falling over 2021, rules of thumb should be reexamined. Given the constraints on Fixed Income (risk control in most portfolios), holding more cash helps to lower the duration risk and volatility of portfolio returns. A solution to lower income is to barbell your risk, hold more equities and hold more cash. In order to maintain balance in achieving long run objectives, this approach is most suited for new cash, rather than any abrupt changes to strategic asset allocation.

2021 is an Extension of Long-Run Trends

For over 30 years, generating consistent returns has meant higher levels of portfolio complexity and volatility – what investors face now, is no different. See the chart below.

Finding a 7.5% return in 1989 was as simple as holding 25% of your assets in US Treasuries, and the remainder of your money in Cash (yielding an annualize 4% in vol). Talk about the easy days! Just to maintain that same 7.5% level of return in 2020, modern portfolios have had to increase both complexity and risk. Today a standard blended portfolio holds 6 or more asset classes, in both domestic and international markets, with both public and private assets.

All this generates the same expected return but at the cost of increasing annualized volatility in the portfolio to 18%.

Source: Callan, Alaska Permanent Capital Management

Looking Forward: What Separates the COVID Cycle From Other Recoveries is the RISE in Investible Capital (Income & Savings)

The economic backdrop in the US and Globally is accelerating in 2021 and 2022, helping drive asset inflation and valuations. Less often followed are trends in capital formation in the form of savings and income, and how this feeds back into market valuations.

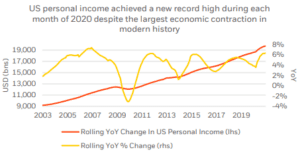

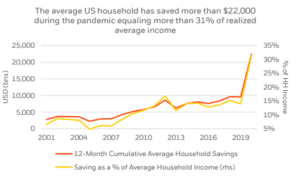

Take a moment to look at the chart below, courtesy of Blackrock. US personal income recorded a new high each month of 2020, despite the largest economic contraction in modern history. Savings of US households (relative to income) jumped to 31%, well beyond either the 2001 or 2008 recessions. These two trends suggest there is pent-up supply of investible capital, when coupled with growth in the economy leads to additional flow into financial assets.

This increase in flow will push market prices up, even in an environment where valuations appear stretched compared to history.

Source: Blackrock, Bloomberg

So, Where Can Money Go if Rates are Unattractive?

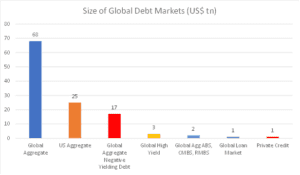

Investible capital needs to find a home, think of it as an animal always seeking out the highest risk adjusted return – but the fixed income outlook in 2021 has presented challenges. Clients need risk-control assets to anchor a portfolio in turbulent times, but this is not as simple as swapping to another debt market (like High Yield) should US Treasuries and International Sovereigns prove unattractive.

Depth of market becomes a barrier as seen in Chart 4 below. Even when they are combined, Corporate credit, municipals and even private markets are just not large enough to substitute for the volume of US AGG.

Source: Bloomberg, JP Morgan, Blackrock, Alaska Permanent Capital Management

Barbelling the Risk (with Cash and Equities) is One Solution

Fixed income will always have a positive duration risk and a positive vol impact on a portfolio. In a rate rising environment, which is a probable scenario for the next few years, a duration impact (negative price returns) can overwhelm the income effect yielding negative total returns. It is a risk to portfolios in early expansions as real yields and inflation rise from countercyclical fiscal policy and a widening fiscal deficit.

Cash has zero duration risk and zero volatility — so you can reduce this negative impact simply by holding more cash.

Since there is no free lunch, the trade off with higher cash levels is have less defined income (i.e. the coupon of the bonds).

At the time of writing, the income difference between cash and 10y UST is 1.7% roughly. You can help close that gap with an additional allocation to equity or alternative assets. Our preference on the multi-asset team is for Equities (where we hold a 2% overweight to our strategic target) and Infrastructure (a 1% overweight), but you could also choose other risk assets as well so long as the increased risk allocation gets back some of the expected return. A rule of thumb is 20% of the total bond reduction held in diversified equities, with the remainder in Cash for risk control.

Richard Cochinos, CFA®, CAIA®

Senior Portfolio Manager

Multi-Asset Strategies

4/12/21