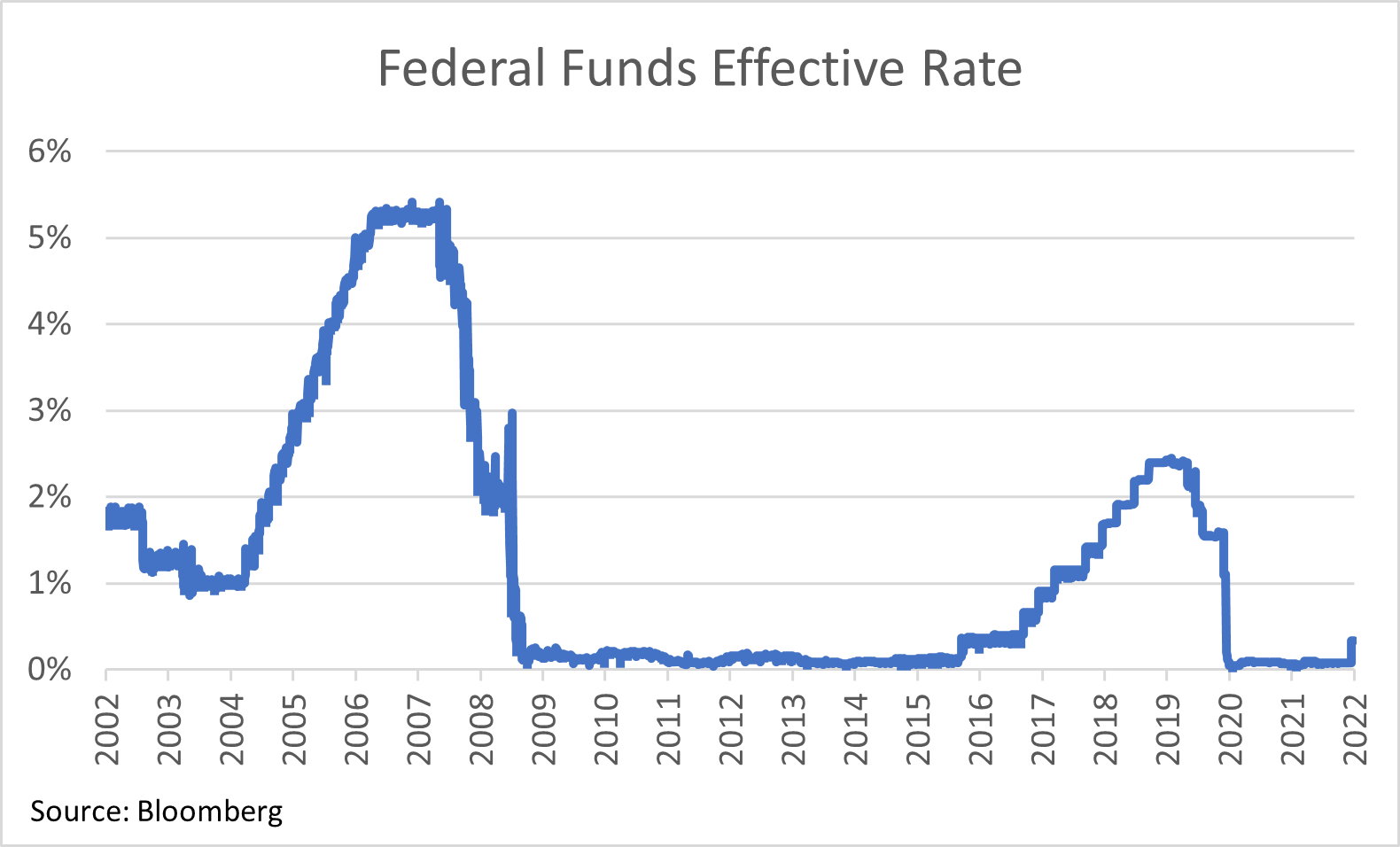

At its March 16, 2022, meeting, the Federal Reserve increased the Fed Funds rate by 0.25%. The new target range is 0.25% to 0.50%. This was the first in what is expected to be a series of hikes that will occur throughout 2022 and likely into 2023 as well.

In the last 20 years there have been two other rate-hike cycles. In the two years from mid-2004 to mid-2006, the Fed Funds rate went from 1.00% to 5.25%. This was accomplished in a steady series of seventeen quarter-point rate increases. The second rate-hike cycle started in December 2015 with rates near zero. After an initial bump up to 0.50%, they followed through with increases at a rate of four 0.25% hikes each year until December 2018 when it reached a peak level of 2.50%.

The Fed Funds rate is the interest rate at which banks lend money to each other on an overnight basis. This creates something of a floor for short-term interest rates. While the current level of this short-term rate is important, the direction and magnitude of future Fed Funds rates is even more significant. It is the basis for longer term loans and for a host of products ranging from retail borrowings such as car loans and mortgages, to institutional debt such as municipal and corporate loans.

The Federal Reserve has six more meetings scheduled in 2022 (May 4th, June 15th, July 27th, September 21st, November 2nd and December 14th). Current market expectations are for at least a quarter point rate increase at each of these meetings. This means that Fed Funds could end the year at 2% or higher. Using prior rate cycles as a guide, we still have a long way to go before Fed Funds reaches its peak rate for this cycle.

Fed has two levers for Monetary Policy – It is exercising one, and will soon implement the other

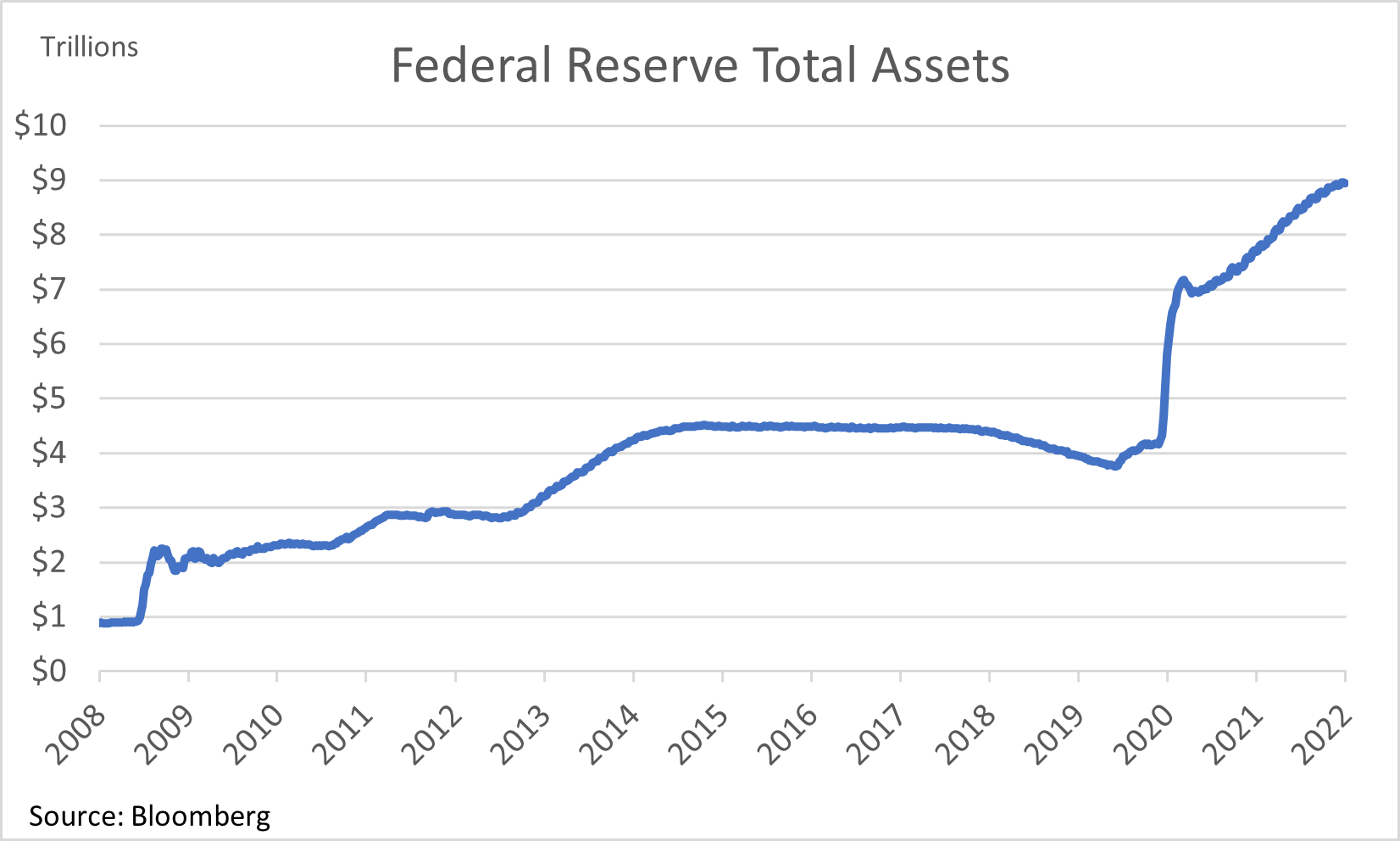

Increasing the Fed Funds rate is only one of the tools the Federal Reserve has at its disposal to help bring down inflation. Perhaps just as important is the Fed’s Balance Sheet.

Throughout the pandemic, the Fed was buying debt instruments. This had the effect of injecting liquidity into the US financial system and helped mitigate the pandemic’s economic impact. It also caused the Fed’s Balance Sheet to increase. Currently total assets on the Fed’s Balance Sheet are around $9 trillion. To put that number in context, that’s approximately the size of the 2022 Gross Domestic Products (GDP) of Japan and Germany combined.

Growing the balance sheet has come to an end as the Fed is no longer making purchases. The question of when the Fed will start to decrease its assets and at what rate (thereby removing liquidity and slowing down the engines that drive economic growth) is one that market participants will be following closely.

We believe that moving Treasury and Mortgage securities from the Federal Reserve balance sheet to the open market will provide a small tailwind to increasing rates.

The Fed will be working these two levers (interest rates and balance sheet) in an effort to bring inflation back down towards its long-term target of 2%. It will not be an over-night process. Current Wall Street economist forecasts are for inflation to drop from 7.7% in the first quarter of 2022 to 2.5% in the second quarter of 2023. The Fed will attempt to do this without causing a recession by being overly restrictive with its monetary policy. If successful, they will have achieved a “soft landing” which was last accomplished in 1994.

Paul Hanson, CFA®

Senior Portfolio Manager

4/4/2022